From 2mm to 2cm: Amorphous Alloys Break Through Thickness Limit

Amorphous alloys are like carbon fiber in the year 2000—a luxury today, but an essential material tomorrow.

Amorphous alloys are like carbon fiber in the year 2000—a luxury today, but an essential material tomorrow.

While traditional metals maintain orderly crystalline structures, a revolutionary material is reshaping materials science: amorphous alloys, often called "liquid metal" by sci-fi enthusiasts. With their chaotic atomic arrangement, they deliver extraordinary properties surpassing conventional metals—ultra-high strength (1,600-2,200 MPa), extreme hardness (500-600 Hv), exceptional elastic limit (2%), and superior corrosion resistance.

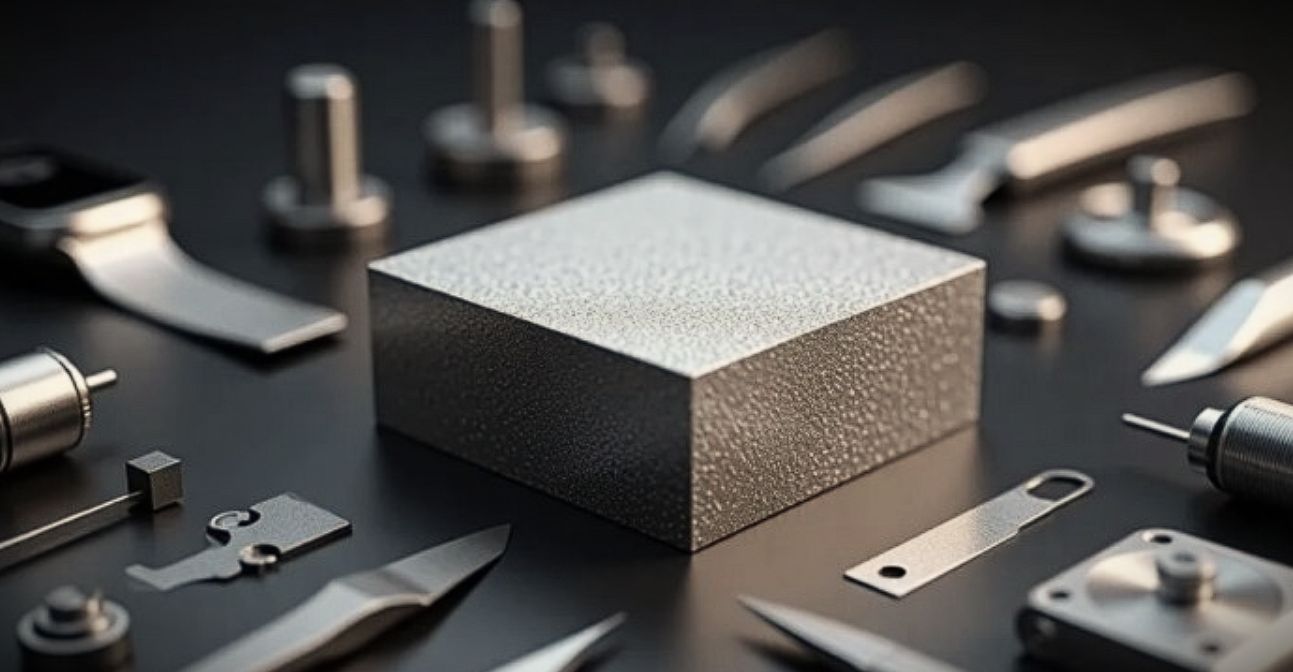

After three decades of R&D breakthroughs, amorphous alloys have evolved from Hitachi Metals’ micron-thin ribbons to Chinese enterprises achieving 2cm-thick blocks via million-degrees-per-second cooling. Increasing thickness presents exponentially greater challenges, representing entirely distinct technical regimes.

As thickness capabilities grow, industrial applications explode: foldable phone hinges, smartwatch casings, motor housings, artificial bones, and even brain-computer interface electrodes. This once lab-bound "liquid metal" is fulfilling its promise to transition from luxury to necessity.

The Atomic Code of Amorphous Alloys

The story began with the September 3, 1960, Naturepaper "Non-Crystalline Structure in Solidified Gold-Silicon Alloys." U.S. Professor Duwez serendipitously discovered that molten alloy cooled at ~1,000,000°C/sec "freezes" atoms into disordered states before crystallization—creating humanity’s first amorphous alloy. Controlling this atomic chaos requires overcoming thermodynamic and kinetic barriers—akin to sculpting ice during a volcanic eruption.

At the microscopic level:

- Traditional metals arrange atoms in disciplined crystalline lattices.

- Amorphous alloys resemble atomic improvisation—no repeating patterns ("long-range disorder"), observable even at nanoscale. Atoms remain "frozen" in liquid-like randomness.

This disordered structure unlocks unparalleled properties:

- Ultra-high strength: 1,500–2,200 MPa (lab record: 6,000 MPa), exceeding steel (100–1,300 MPa), stainless steel (200 MPa), and titanium alloys (900 MPa).

- Extreme hardness: 500–600 Hv (lab record: 1,800 Hv), surpassing stainless steel (200 Hv) and titanium (400 Hv).

- High elasticity: Elastic limit up to 2% (theoretical max: 4.2%), versus 0.6% for titanium/stainless steel.

- Corrosion resistance: Absence of grain boundaries prevents corrosion pathways.

- Lightweight: 13–34% lighter than stainless steel of comparable composition.

- Additional properties: Antibacterial performance, biocompatibility, catalytic activity, and adsorption capacity.

Three-Decade Evolution: From Micron Ribbons to Centimeter Blocks

(1) 2000s: Micron-Thin Ribbons for Power Cores

Initial industrialization used iron-based alloys via "melt-spinning," producing 20–80μm ribbons. These replaced silicon steel in transformer cores, cutting no-load losses by 70–80%.

(2) 2010s: Millimeter Strips for Thin-Wall Applications

Zirconium-based alloys emerged, processed via "vacuum die-casting" to achieve ≤2mm thickness. High costs limited use to premium 3C components.

(3) 2020s: Centimeter Blocks Enable Broad Applications

Pioneering firms broke the cm-threshold using zirconium-, titanium-, and copper-based alloys. Advanced "atmosphere-protected die-casting" boosted yields and cut costs, expanding into consumer electronics, medical devices, machinery, and aerospace.

Global Race: Ribbon Dominance vs. Bulk Material Breakthroughs

Amorphous alloys divide into two domains with distinct technologies, applications, and market leaders:

- Ribbons (iron-based): Primarily for power distribution (e.g., transformer cores).

- Bulk materials (zirconium/titanium/copper-based): For structural components.

(1) Ribbon Production: China Leads

Japan’s Hitachi Metals (1977 pioneer) dominates globally with 100,000-ton annual capacity (20% market share). China now produces 70% of global supply:

- Qingdao Yunlu: 100,000+ ton capacity; 40% global share.

- Ametek: 50,000+ ton capacity; 10% global share.

2024 China Data:

- 14.5万吨 ribbon output (+23.9% YoY).

- ~90,000 tons exported (primarily to Southeast Asia).

- Nanocrystalline alloy (ribbon derivative): 40,000-ton output (60% global share).

(2) Bulk Materials: Immense Potential

U.S.-based Liquidmetal Technologies pioneered zirconium/titanium bulk alloys. Challenges like brittleness, machining difficulty, and high costs (e.g., zirconium alloys: >¥2,000/kg) limit commercialization. Current domestic market: ~¥1 billion, projected to grow exponentially.

Chinese innovators include:

- Jiangsu Chaos New Material Technology

- Changzhou Shijing Liquid Metal

- Dongguan Yihao Metal Materials

- Shanghai Chisheng Metal Technology

Notable development: Huawei and Jiangsu Chaos co-patented zirconium-based amorphous alloy tech for foldable device hinges (2025).

Technical Breakthrough: The 2cm Threshold

"Full-Cycle Atmosphere-Protected Die-Casting." This process:

- Ensures uniform million-degrees-per-second cooling.

- Maintains ultra-low oxygen environments.

- Solves core-cooling challenges for thick sections.

- Delivers ±0.02mm dimensional accuracy (surpassing MIM, rivaling CNC).

- Eliminates secondary processes (sintering/heat treatment).

Key properties:

- Seawater immersion: Zero corrosion after 2 years.

- 20% hydrochloric acid: Withstands 3-month exposure.

- Corrosion resistance: 10× superior to 316 stainless steel.

Applications Ignite: A Billion-Yuan Market

Foldable devices lead adoption:

- Huawei’s Mate X (2019) and Mate XTs (2025) use zirconium hinges.

- Amorphous hinges survive 500,000+ folds (2× traditional metals).

- 2025 China foldable shipments: 9.47M units (hinge material market: ~¥1 billion).

Expanding applications:

- Automotive: Latches, handles, hinges.

- Wearables: Smartwatch casings.

- Industrial: Motor housings (15–20% lighter), harmonic drive flexsplines.

- Medical: Bone implants (50% faster osseointegration), tremor-free surgical tools.

- Neurotech: Brain-computer interface electrodes.

Market forecast: Zirconium bulk alloy demand to grow 30–40% annually, exceeding ¥10 billion in 3–5 years.

The Centimeter Era Begins

From Duwez’s accidental discovery to Hitachi’s ribbon dominance, and now China’s bulk-material breakthroughs, amorphous alloys have entered their "Centimeter Era." No longer lab curiosities, they are becoming essential enablers across industries—driving lighter, stronger, smarter futures.

As Zhang Qidong (Jiangsu Chaos) observes: "Amorphous alloys today mirror carbon fiber in 2000—tomorrow’s necessity born from today’s luxury."

Baohui Steel limited

Baohui Steel Limited has established itself as a leading exporter of oriented silicon steel and amorphous materials, with a strong client base in the transformer industry. Thanks to their unique properties, amorphous iron cores are now reshaping the development landscape of the transformer sector. As a transformer manufacturer or processor, we are equipped to provide you with comprehensive material solutions and processing services, empowering you to gain a competitive edge in this rapidly evolving industry.